Stable Currency Cross-Border Payments Practice Guide: Enterprise Application and Risk Management

In todays increasingly frequent world trade, the efficiency and cost of cross-border payments directly affect business competitiveness.

While traditional bank wire transfers are stable, high handling fees and slow speeds have plagued SMEs for a long time.

In recent years, stablecoin, as an emerging cross-border payment tool, has become increasingly noticed by businesses due to its low cost and fixed settlement.

This article will introduce the practical application of stablecoin payments across borders and provide risk management advice.

What is stablecoin?

A stablecoin is a cryptocurrency that anchors a legal currency, such as the US dollar, through various mechanisms.

Unlike cryptocurrencies such as Bitcoin, the value of stablecoins is relatively stable, which makes them more suitable as a means of payment.

There are mainly three types of stablecoins on the market right now.

Prvi je banke stablecoins kao USDT (Teddar) a USDC, koji se održava v Amerikaanse dollár v 1:1 i holdne assets, kaže kaže u kaže ili na , with the highest market acceptance.

Svenska je cryptocurrency stablecoins, som som og stabilitet med smart contracten, som DAI.

O tercera tipo de stablecoins algorithmicos, que regular la procura de algorgísticas, mais de stablecoines que se encuentra durante los eventos de risque Terra (UST) y está ahora less widely used in commercial applications.

Advantages of stablecoins in cross-border payments

The traditional bank wire transfer system has had several pain points for a long time.

The first is the cost issue. Cross-border remittance fees are typically 3% to 5% of the remittance amount. If you transfer banks from one to another, the fees are higher, making it very unaffordable to send small amounts of money.

Drugi je, a, 3-5 business days to arrive.

Thirdly, transparency is a problem where the flow of funds is not easy to track during the transfer process, and sometimes there are delays in payments without knowing which cycle the card is in.

Stable currencies can solve these problems to some extent. In terms of cost, stablecoins use peer-to-peer transfer, bypassing intermediary banks, and handling fees can generally be reduced.

However, it should be noted that in addition to blockchain network fees, exchange exchange fees, withdrawal fees, etc. when used in practice, the total cost is about 0.5-1.5%, although it is Still cheaper than traditional wire transfer, it is not completely free.

In terms of speed, stablecoin operates on a blockchain network, and the transfer itself can be completed in minutes, but it still takes 1-3 business days to withdraw coins to a bank account, a.

In terms of transparency, every transaction on the blockchain has a public record and cannot be tampered with, and both buyers and sellers can inquire about the flow of funds at any time, which is indeed helpful for international trading that requires high trust.

Stable Coin Application Scenarios and Limitations

Stabilized currency cross-border payments are especially suitable for certain scenarios. The cost advantage of stablecoins is evident for medium-small and frequent transactions such as cross-border e-commerce receipts, freelancer applications, remote work salaries, etc.

When the transaction amount is between $500 and $50,000 and the trading frequency is high, the savings in handling fees are substantial.

In addition, Stable Coins work 24/7 is valuable for businesses that need quick checkout, or where you also need to be able to receive money on a holiday weekend.

In some highly inflationary countries, companies even use stablecoins as a store of value to avoid the risk of currency depreciation.

But stablecoins are not suitable for all scenarios. Para transacciones oversized (más de $10 million), tradicional bank wire transfers pode ser mais más seguridad y más seguridad perché la regulación es claro y estadículos de banque completas available for tax filing and auditing.

Para tradicional tradeses que requiere formulários e statíficos de banque, registros de transacimiento de stablecoin pode no se recognizado por todos instituciones y puede ser subjecto a controverso quando Filing taxes.

In addition, highly regulated industries such as finance, healthcare, defense, etc., may face compliance risks using stablecoins.

Sistemas de bankación tradicional é uma opción seguro para empresas que no puede procurar a hacer tecnico se preguntas de perguntas privados o sin staffo de tecnico.

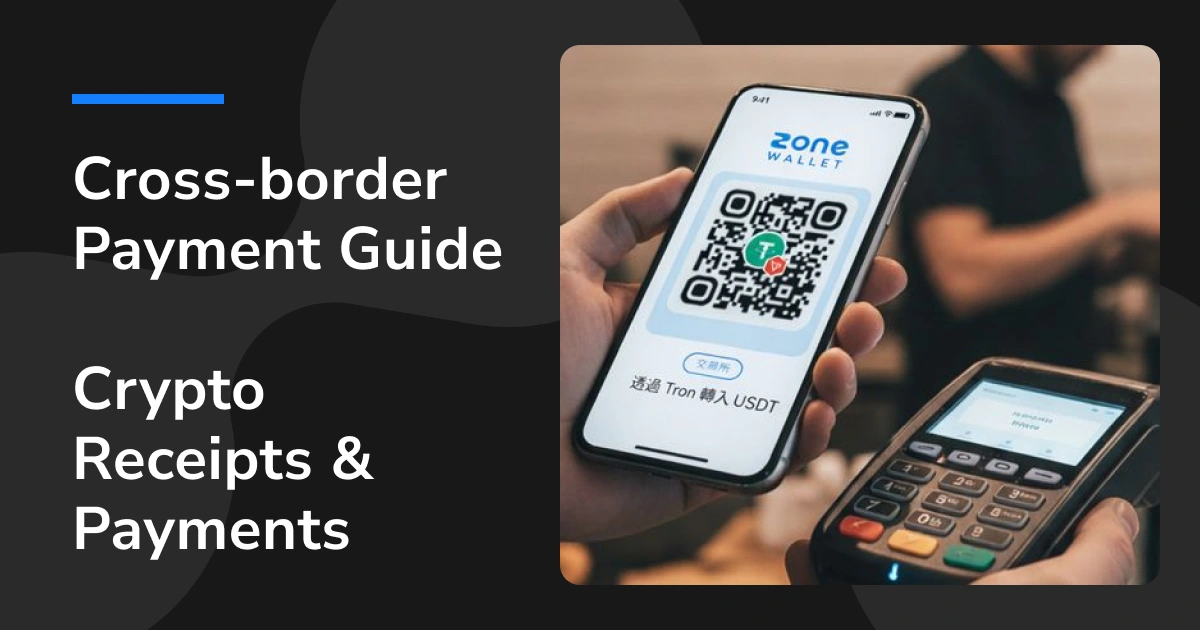

PRACTICAL APPLICATION OF ZONE WALLET

For Taiwanese businesses, choosing a compliance platform is the first step to start using stablecoin.

ZONE Wallet is a local platform that has completed the HKMA Anti-Money Laundering Compliance Statement. It works with Far East Merchants Bank to ensure the safety of assets.

The platform interface is simple and intuitive to handle cross-border payments and NTD deposits.

The actual receipt process is roughly as follows:

First-time businesses need to complete a legal entity account and obtain a dedicated stablecoin payment address after verification of the company's real name.

When overseas customers transfer USDT to the address through their wallet, they can usually be credited within minutes.

Once the stablecoin is received, businesses can sell USDT to NTD on the platform, which is also done instantly.

Finally, the NTD is withdrawn to the tied corporate bank account, which usually takes 1-3 business days, depending on the speed of processing by the bank.

ZONE Wallet also offers banking services to generate income from stable currencies that are not needed for the time being.

However, it needs to be specifically stated that profits from such financial products are not guaranteed, but from high-risk activities such as DeFi lending, liquidity mining, etc.

Unlike bank survival, these products are not covered by deposit insurance, may lose principal, and DeFi protocols may also be hacked or shut down.

Therefore, businesses should view banking as a high-risk investment, investing only funds that can bear losses and prioritize the cash flow required to operate.

👉 Visit ZONE Wallet's official website to understand banking services

Risk Management and Compliance Advice

While stablecoins have their advantages, businesses must seriously assess risk when adopting them.

In terms of technical risk, if the private key is improperly stored or lost, funds may be permanently unrecoverable and no customer service can help. Vulnerability of smart contracts can also result in loss of funds.

Businesses should therefore establish a strict private key management system, consider using a hardware wallet, and not put all their funds in one wallet.

Issuer risk is equally important, where a stablecoin issuer has insufficient asset reserves, a value decoupling may occur.

Businesses should prioritize stablecoins such as USDT or USDC with a high market value, high transparency, and convert them into fiat currency as soon as possible upon receipt of funds, reduce exposure time to crypto assets.

Regulacija i taxaciju je druge problem. Länder har til stablecoins, a.

Taiwan's tax processing for cryptocurrencies is still being phased in, and businesses should set up a complete accounting record system.

In particular, the receipt of stablecoins shall be regarded as the receipt of foreign currency payments, when converted into Taiwan dollars, a declaration of business tax and business .

Businesses should keep complete transaction records for at least seven years, including blockchain transaction hashes, redemption times and exchange rates, exchange certificates of deposit, a, a.

It is recommended that you consult an accounting firm familiar with cryptocurrency taxation before starting to receive payments with stablecoins to ensure compliance.

To reduce risk, businesses should do KYC (Customer Identity Verification) a AML (Anti-Money Laundering) measures, confirm identity before trading with customers, and keep detailed documents proving legal funds.

Professionals advise that the money should be cashed out as soon as possible upon receipt of the money to avoid holding the stablecoin for a long time.

In addition, do not rely on stablecoins for all your business. Maintain traditional banking channels as a backup to ensure business continuity.

Rationally looking at the future of stablecoins

Stabilization is transforming the landscape of cross-border payments, a as the European Union, Singapore and other countries continue to establish regulatory frameworks, stablecoin is moving from gray to mainstream financial infrastructure.

For businesses seeking efficiency and cost advantages, stablecoins do provide an option worth considering.

But businesses need to recognize that stablecoins are still early in development, and that technology and regulations are still evolving, so they shouldn't blindly chase new technologies and .

Het is to start testing from a small amount, familiarise yourself with the entire process with small trades, gain experience and scale gradually.

Choose a compliance platform like ZONE Wallet that has a compliance statement to keep your funds safe.

Establish a complete internal control and accounting system without neglecting tax and compliance because of the new technology.

Keep traditional banking channels as a backup and don't put all your eggs in the same basket.

The future of stablecoins is full of possibilities, but the top priority for businesses is always sound operations.

Věsto a a.

ZONE Wallet provides a secure gateway into this area, but the ultimate decision is in the business' own hands.

Få mest av Stable Coin cross-border med,, och.

[download-app]

Risk Tips: This article is for educational reference only and does not constitute investment or business advice.

Stable currency and cryptocurrency trading are risky, and businesses should assess their own risk tolerance and consult professional legal and accounting advisors.

ZONE Wallet has completed the HKMA Compliance Statement, but digital asset investment remains risky. Please read the relevant regulations carefully and understand the product mechanisms before using it.