What is Cross-Border Payment? An international payment solution for businesses and individuals

With the increasing frequency of global business activity, cross-border payments have become an indispensable financial tool for modern businesses and individuals. Whether it's cross-border purchasing, overseas investment, international trade, or individual overseas spending, understanding how cross-border payments work and choosing the right payment method can greatly increase transaction efficiency and reduce costs. This article will give you an in-depth look at the different aspects of cross-border payments to help you make the best payment decisions.

What is Cross-Border Payment? Learn more about the basic concepts of international payments

Cross-border payments are money transfers and payment services between different countries or regions. When businesses need to pay overseas suppliers or individuals need to send money abroad, they need to complete transactions through a cross-border payment system. This payment method involves multiple currencies, different financial systems, and national regulatory requirements, making it more complicated than domestic payments.

Traditional cross-border payments rely primarily on inter-bank wire transfer systems, such as the SWIFT network, but with the development of fintech, there are now more diverse payment options. Cross-border payments include not only B2B business transactions, but also B2C consumer payments, C2C personal transfers, and various application scenarios for digital commerce.

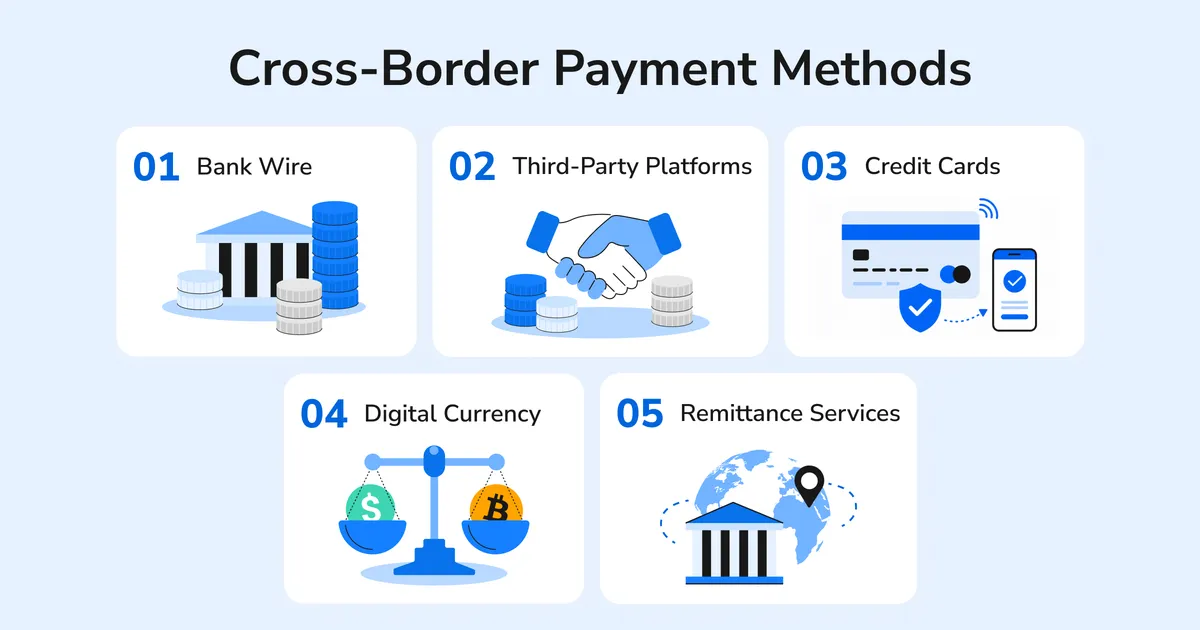

Comparison Analysis of Major Cross-Border Payment Methods

There are many cross-border payment methods on the market, each with its specific advantages and applicable scenarios. Choosing the right payment method requires consideration of a number of factors such as transaction amount, timeliness, processing fees, security, and more. Below we will detail the various main payment methods and their features.

Wire Transfer

BANK WIRE TRANSFER IS ONE OF THE MOST TRADITIONAL AND MOST STABLE CROSS-BORDER PAYMENT METHODS. Through the SWIFT network, funds can be transferred securely between major banks around the world. This method is suitable for large transactions, very secure, but longer processing time, usually 1-5 business days, and relatively high processing fees, usually between $20-50.

pros: Highly secure, global banking network coverage, suitable for large transactions

shortcomings: LONG PROCESSING TIME, HIGHER PROCESSING FEE, UNTRANSPARENT EXCHANGE RATE

Third-Party Payment Platforms

Third-party payment platforms such as PayPal, Wise (formerly TransferWise), Remitly offer more convenient cross-border payment services. These platforms typically offer more transparent exchange rates and lower processing fees, and faster processing speeds than traditional banks. Especially suitable for SMEs and personal users, supports multiple currencies and user-friendly interface.

pros: Easy operation, fast speed, transparent exchange rate, relatively low handling fee

shortcomings: Some platforms have restrictions on the amount of transactions, and the quality of customer service is uneven

Credit Card Payment

Credit cards are one of the most common payment methods for cross-border e-commerce and overseas consumption. The issuing bank converts the consumption amount into the cardholder's local currency at the current exchange rate and may charge an overseas transaction fee of 1.5%-3.5%.

pros: High convenience, wide acceptance, consumer protection mechanism

shortcomings:Higher processing fees, exchange rates may not be advantageous

Digital currency payments

Cryptocurrencies like Bitcoin, Ethereum, as well as stablecoins bring new possibilities for cross-border payments. Digital currency payments are characterized by decentralization, 24-hour operation and relatively low processing fees, especially with significant advantages for large cross-border transfers. Stable currencies such as USDC, USDT and other blockchain technology enable cross-border transfers to be completed in minutes at a cost of just a few dollars.

pros: Fast transaction speed (minute level), low processing fee, no bank hours limit

shortcomings: Risk of price volatility, regulations are not yet clear, technical thresholds are higher

International Money Transfer Companies

Traditional international money transfer companies such as Western Union, MoneyGram, have physical locations around the world and offer cash transfer services. This type of service is especially suitable for users who do not have a bank account or where urgent money transfers are needed.

pros: Wide number of global locations, cash transactions, fast checkout

shortcomings:Higher processing fee, exchange rate is not advantageous

Cross-border Payment Channel Selection Guide

Choosing the right cross-border payment channel requires a number of factors to be considered in combination. Different payment channels have advantages, and businesses and individuals should make choices based on their needs.

| Payment Channel | Processing Time | Fees | Ideal Use Case | Security Level |

|---|---|---|---|---|

| Wire Transfer | 1-5 Business Days | $20-50 + Intermediary Fees | Large B2B trades, Real estate, Investments | Extremely High |

| PayPal | Instant - 1 Business Day | 2.9%-4.4% + Fixed Fee | E-commerce, Cross-border shopping, Service payments | High |

| Wise | Minutes - 2 Business Days | 0.4% - 2% | Personal transfers, SMB payments | High |

| Credit Card | Instant | 1.5% - 3.5% | Overseas spending, Hotel/Ticket booking | High |

| Stablecoins | Minutes - Few Hours | $1 - $5 USD | Large cross-border transfers, Tech industry | Moderate |

| Western Union | Minutes | Variable (Based on amount) | Urgent remittance, Unbanked individuals | Moderate |

Enterprise User Considerations

Businesses need to focus on compliance, financial security, cost control, and operational efficiency when choosing a cross-border payment channel. Large enterprises often prefer bank wire transfers to ensure financial security and compliance; SMEs may be more inclined to use third-party payment platforms to reduce costs and streamline operations.

- Evaluate monthly transaction volume and single transaction amount: Businesses with large monthly transactions should negotiate better rates with payment service providers

- Confirm payment channels comply with regulatory requirements: Different countries have different control rules for the entry of funds. Please know in advance

- Consider System Integration Capabilities: Choose a plan that can be networked with an existing ERP or financial system for automated reconciliation

- Assess customer acceptance: Choose a commonly used local payment method based on the payment habits of target market customers

- Create a backup plan: Avoiding a single pipeline failure that leads to business interruption

Individual User Selection Suggestions

Individual users often pay more attention to convenience, cost, and speed when choosing cross-border payment channels. There are different payment channels for different needs for overseas purchases, study transfers, family remittances, etc.

| Use Case | Recommended Channel | Reason for Choice |

|---|---|---|

| Overseas E-commerce Shopping | PayPal, Credit Card | High convenience and consumer protection |

| Study Abroad Tuition | Wire Transfer, Wise | Large amounts; ensures secure arrival of funds |

| Small Family Remittances | Wise, Remitly | Low cost and fast processing speed |

| Emergency Remittance | Western Union | Instant arrival with extensive global locations |

| Large Cross-border Investment | Wire Transfer, Stablecoins | Security or cost considerations |

Cross-border payment cost analysis and optimization strategy

The cost of cross-border payments includes handling fees, exchange rate spreads, intermediary fees, and many other items. Understanding these cost structures helps you choose the most economical payment plan. In general, the total cost will not be equal to 1-5% of the transaction amount, but with the right strategy, these costs can be reduced effectively.

Major Cost Composition

- Fixed handling fee: Fixed fee charged per transaction, such as $20-50 for bank wire transfer

- Percentage Handling Fee: Calculated as a percentage of the transaction amount, e.g. 2.9%-4.4% for PayPal

- Exchange Rate Spreads: Spreads accrued by servicers on exchange rates, usually hidden in quotes

- Middle Line Fees: Additional fees may be charged by intermediary banks during bank wire transfers

- Receipt Line Fees: Deposit fees that may be charged by the receiving bank

Practical tips for cost optimization

- Compare Total Costs for Different Platforms: Don't just look at transaction fees, calculate exchange rate spreads

- Select Local Currency Settlement: Try to use the local currency of the receiving party to avoid secondary exchange

- Consider Batch Processing: Combine multiple small payments into a single large payment, reducing the transaction cost ratio

- Make use of exchange rate tools: Set exchange rate reminders to trade at a favorable exchange rate

- Negotiate with financial institutions: Business customers can strive for better rates based on transaction volume

- Create a Diversified Payment Pipeline Portfolio: Best way to use for different types of transactions

- Consider a stablecoin solution: For large cross-border transfers, stablecoins can significantly reduce costs

Cross-border payment risk management and compliance highlights

Cross-border payments involve multi-country regulations, and businesses and individuals alike need to be aware of the risks involved and compliance requirements. The main risks include exchange rate risk, operational risk, compliance risk and credit risk. Establishing a sound risk management mechanism is critical to ensuring smooth cross-border payments.

Main risk types

Exchange Rate Risk: EXCHANGE RATE FLUCTUATIONS MAY AFFECT THE ACTUAL PAYMENT AMOUNT FROM TRANSACTION INITIATION TO SETTLEMENT COMPLETION. Businesses can hedge through financial instruments such as forward contracts, options and other financial instruments.

Operational Risks: Human errors, system failures, or payment message errors may result in payment delays or failures. Establishing standardized workflows and multiple verification mechanisms can reduce this risk.

Compliance Risks: Violations of laws such as money laundering, foreign exchange controls can result in fines, account freezes, and even criminal liability.

Credit Risk: The payee may not be able to fulfill contractual obligations or the payment service provider may have financial problems.

Regulatory Compliance Considerations

Countries have specific regulatory requirements for cross-border payments, including anti-money laundering (AML), Know Your Customer (KYC), foreign exchange controls, and more. Businesses need to ensure their chosen payment channels comply with relevant regulations and establish appropriate internal controls. Individual users also need to be aware of the restrictions involved to avoid tactile approaches.

- Complete the necessary authentication and data provisioning procedures: Prepare relevant documents in advance to speed up the review process

- Comply with foreign exchange controls and reporting requirements in different countries: Understand remittance limits and reporting thresholds

- Maintain complete transaction records and related documents: Use in preparation for verification or dispute handling

- Regular updates on relevant regulatory changes: Continued evolution of regulatory policies in different countries requires constant attention

- Choosing a Payment Service Provider with Care: Select reputable and compliant service providers

Future Trends and Development Directions for Cross-Border Payments

The cross-border payments industry is rapidly changing, with the application of new technologies and the changing regulatory environment driving industry innovation. Emerging technologies such as central bank digital currencies, blockchain technology, artificial intelligence are reshaping the landscape of cross-border payments to provide users with a faster, cheaper, and more secure payment experience.

Stable Currency and Central Bank Digital Currency (CBDC)

Stabilization has shown great potential in the cross-border payments space, with MasterCard acquiring stablecoin infrastructure company BVNK for $18 billion, demonstrating the high importance of traditional financial giants in the field. At the same time, central banks are actively developing digital currencies, and China's digital renminbi, Europe's digital euro, etc. will have a profound impact on the future cross-border payment landscape.

Instant Payment System

More and more countries and regions are establishing instant payment systems and promoting cross-border connectivity. In the future, cross-border payments can be made as fast as domestic transfers, greatly improving the efficiency of money turnover.

Blockchain and Smart Contracts

Blockchain technology greatly simplifies the clearing and settlement process for cross-border payments, reducing intermediate loops. Smart contracts enable conditional payments, automated reconciliation, and more to reduce operating costs.

Regulatory Technology (RegTech)

The development of regulatory technology will simplify the compliance process and reduce compliance costs. Automated KYC, transaction monitoring, risk assessment, and more tools will make cross-border payments safer and more efficient.

Practical Operating Advice and Best Practices

A successful cross-border payment strategy requires a combination of practical experience and best practices. Businesses or individuals should establish a systematic approach to payment management, including supplier assessment, cost monitoring, risk management, and more.

Enterprise Cross-Border Payment Best Practices

- Establish a supplier evaluation system: Regularly review payment provider performance, rate changes, and service quality

- Establishment of dedicated staff to manage cross-border payments: Ensure that there are professionals to continuously optimize payment strategies

- Create an emergency plan: Prepare backup payment channels to deal with major pipeline failures

- Regular cost-benefit analysis: Continuous optimization of payment strategies to ensure the most cost effective

- Enhance internal education training: Enhance teams' expertise and risk awareness of cross-border payments

Practical Advice for Personal Cross-Border Payments

- Planning ahead: Avoid urgent remittances, compare costs and speeds of different channels in advance

- Make the most of calculation tools: Many platforms offer cost calculation functionality to estimate the total cost in advance

- Pay attention to hidden fees: Keep an eye out for hidden costs, such as exchange rate spreads, and choose the plan with the lowest total cost

- Keep Transaction Records: Save remittance certificates and related documents for occasional use

- Understanding Benefit Protection: Familiar with the dispute handling mechanisms and protection policies of the selected payment channels

epilogue

The selection and management of cross-border payments is a process of continuous optimization. As the business evolves and the market changes, payment strategies also need to be adjusted in due time. It is recommended to regularly review payment costs, efficiency and risks, and keep an eye on the development of new technologies and new services to ensure that the most suitable payment solution is always adopted.

Whether corporate or individual, understanding the various options, cost structures, risk management, and future trends in cross-border payments can help you manage international money flows more effectively and increase your competitive edge in a globalized era.

Cross-border payments should not be a heavy burden in this borderless digital age. Download ZONE Wallet now and start your first step in exploring a new perspective on global finance!

[download app]

※ This article is for reference only, details are based on customer service