What is Digital Currency? A Beginner’s Guide to Crypto Investing

Today in the 21st century, we are experiencing a major change in the form of currency. From physical coins, banknotes, to credit cards and mobile payments, the way people exchange value continues to evolve. And now, “digital currencies” are redefining our financial system in a new way. This article will take you to understand the core concepts of digital currencies and the risks that you must know in a simple way.

What is digital currency?

Digital currency refers to a currency that exists only in digital form and does not have an entity. You can't touch it in your pocket, it exists entirely within the computer network and digital ledger. In fact, it is also the electronic New Taiwan currency that circulates behind our daily internet banking and mobile payments. But the digital currency we are talking about today is more about a new monetary system built on blockchain technology. DIGITAL CURRENCIES HAVE THREE CORE CHARACTERISTICS: INTANGIBILITY, 24-HOUR REAL-TIME SETTLEMENT, AND PROGRAMMABLE AUTOMATED TRANSACTIONS VIA SMART CONTRACTS.

Many people confuse digital currency with blockchain, but blockchain is the underlying technology and digital currency is the application that runs on top of it. Blockchain is like a public ledger shared around the world, with decentralized, unalterable characteristics. This technology solves the “double payment” problem of the digital world, ensuring the uniqueness of each digital asset, allowing digital currencies such as Bitcoin to flow safely without central bank supervision.

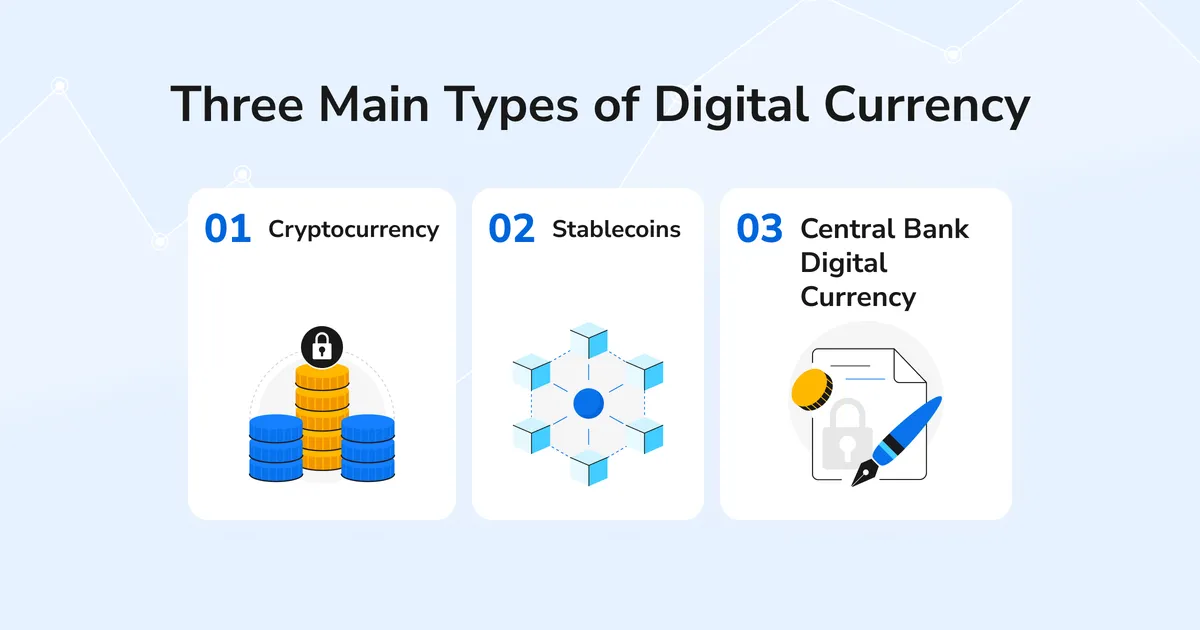

Three main types of digital currencies

Currently, the global digital currency market is mainly divided into three categories.

The first class is cryptocurrency, represented by Bitcoin, issued by private or open source communities, with decentralized, highly volatile characteristics. Bitcoin and Ethereum are currently seen more as tools for storing value rather than everyday payment tools.

The second class is a stablecoin, which was born to overcome sharp price fluctuations, and is usually tied to the dollar 1:1. USDT and USDC, USAT are the most common examples, which serve as a bridge between the French currency and the crypto world.

The third class is the central bank digital currency (CBDC), issued by the central banks of each country, has legal recourse and is actually digital fiat backed by the country's credit. The Chinese digital renminbi and the CBDCs in Taiwan's tests belong to this category.

Advantages and practical limitations

Digital currencies do solve the pain points of traditional finance in some scenarios. The most obvious is the increase in cross-border payment efficiency. Traditional cross-border remittances are expensive and take days, and digital currencies can bypass intermediaries to achieve faster checkout and lower costs in certain situations. In addition, the digital currency market is open 24 hours a year, increasing asset liquidity. But it's also double-edged, and you may be sleeping unresponsive when you fall asleep, which can lead to overtrading and staring stress. Through DeFi protocols, digital currencies can provide automated banking services, but it must be emphasized that these gains are not guaranteed, but come from high-risk activities, possible loss of principal and no deposit insurance.

Despite its advantages, digital currencies are not universal. Extreme price volatility is the most obvious problem, with Bitcoin, Ethereum likely to rise 10-30% in a single day, not suitable for everyday consumption or emergency funds. If you buy coffee with Bitcoin today, and after a week, Bitcoin is up 20%, you will regret “it was early to know that the value was left behind”. This is also why only about 3% of holders have ever used to shop. High technical thresholds are also barriers, requiring understanding of private keys, help words, etc., and errors in operations can lead to permanent loss of assets. Losing a private key is like losing a safe deposit box key, and no customer service can help you get it back. IN ADDITION, REGULATORY UNCERTAINTY, SECURITY RISKS (HACKED EXCHANGES, SCAM PLATFORMS), AND TAX ISSUES (TAX IS REQUIRED TO BE RECORDED ON EVERY TRANSACTION) ARE RISKS THAT BEGINNERS CAN EASILY IGNORE.

How Beginners Get Started Safely

If you are interested in digital currencies, it is recommended to adopt a shallow strategy.

The first step is to choose a compliant platform. It is recommended to choose a local platform registered through the HKMA VASP, such as ZONE Wallet, which supports direct purchase of NTD, funds are held in bank trusts, and provides customer service in Chinese.

The second step is to start with a small amount and invest only the money that you can cover all the losses. We recommend practicing $1,000-$5,000 first. Don't invest blindly for fear of missing an opportunity, and never borrow money.

The third step is to prioritize a stablecoin or fixed-rate strategy with which to pursue Bitcoin's exploits, rather than buying a stablecoin experience first. If you want to allocate Bitcoin, it is recommended to use a regular fixed amount (DCA) strategy, buying a fixed amount monthly to offset the cost.

The fourth step is to take good security measures, turn on two-factor authentication, absolutely do not share private keys with anyone, do not click on unknown links, do not trust “Promise Profit”.

Scams in the field of digital currencies are rampant, and newcomers must be alert. COMMON SCAMS INCLUDE FAKE EXCHANGES OR FAKE WALLET APPS WHERE DEPOSITS CANNOT BE WITHDRAWN AFTER PHISHING PLATFORMS, AND PREVENTION IS TO DOWNLOAD ONLY FROM OFFICIAL CHANNELS. High-yield scams promise 20% monthly returns or guaranteed profits, and most are Ponzi scams. Fake customer service will proactively ask for a password or transfer verification, and regular platform customer service will never do this. Investment group scams are initiated by “teachers” via messaging software to lure you into a fake platform. Do not join an unknown investment group and call the 165 hotline immediately if you are scammed.

Rationally looking to the future

Digital currencies are changing parts of the financial scene, but they are still in their early stages of development and are far from becoming an indispensable infrastructure in life. Technology continues to advance and some applications have shown value, but mass adoption remains challenging. For beginners, the most important thing is rational assessment. Don't be driven by the anxiety of “missed opportunities” or believe that “the best time to enter is always now.” There are both highs and lows in the market, and blind entry may be a constraint. You should learn well first, understand your risk tolerance before deciding whether to participate.

Digital currencies can be part of an asset allocation, but they should never be all. For conservative investors, digital assets may account for only 5-10% of total assets; even entry-level investors should remain diversified. Remember to invest only idle money and keep emergency reserves, and do not let the investment interfere with your normal life. Digital currencies do represent a new way of exchanging value, and it's worth knowing about, but it's important to take risks and choose a compliant platform, starting with a small amount. A cautious attitude will always protect your assets better than blind zeal.

For beginners who want to get started safely, ZONE Wallet is a worthwhile option to consider. The platform has completed the registration of the HKMA VASP. Funds are held in a bank trust, supporting the direct purchase of NTD, and the interface is as simple as using e-banking. A special reminder is that investing in digital assets remains risky, even on compliant platforms. While the financial products offered by the platform may offer returns higher than banks, these gains come from high-risk activities that do not guarantee profitability and no deposit insurance. Before investing, be sure to fully understand the product mechanism and invest only funds that can bear losses.

👉 Learn more about ZONE Wallet's recurring quota service

Disclaimer: This article is for educational reference only and does not constitute investment advice. Digital currencies are high-risk assets, prices fluctuate sharply, and investors may lose all their capital. Please only invest in funds that can bear the full loss, do not borrow money, and choose a compliant platform registered with HKMA VASP. The HKMA reminds: “Virtual assets are non-currency and are not covered by security mechanisms such as deposit insurance. Virtual asset trading is highly risky and investors should be aware of the risks and invest with caution.”

.jpg)